Since the BRICS summit in July 2014 in Brazil, when five developing member countries announced the establishment of the New Development Bank (NDB), there has been widespread media coverage on regional connectivity. One major step forward was in October 2014, when 21 Asian countries signed a Memorandum of Understanding (MOU) on the establishment of the Asian Infrastructure Investment Bank (AIIB) to fund infrastructure projects. The issue gained momentum during the Asia Pacific Economic Cooperation (APEC) Summit in Beijing, as well as at the G-20 Summit in Brisbane, both held in November 2014.

These high-level events brought China to the forefront of the regional connectivity drive. Besides putting together a finance mechanism, China also proposed two infrastructure projects – the New Silk Road, connecting China to Western Europe via Central Asia, and the Maritime Silk Route from China’s eastern seaboard (Quanzhou in Fujian province) to Venice, connecting the ports of Indonesia, Malaysia, India, Sri Lanka, Kenya and Greece. It also re-visited and promoted the idea of a Free Trade Area of the Asia-Pacific (FTAAP) during the APEC Summit.

But why is China taking a leadership role in developing the agenda of infrastructure development and its financing? This paper tries to address the question of China’s connectivity drive as a three-pronged strategy to commensurate its economic rise: disclosing the physical routes; planning the financing; and exploring the feasibility of the routes through increased trade and investment. It justifies the increased discussion on connectivity and the role of AIIB as a self-help mechanism led by Asia’s developing countries, particularly China, to match the shift of global economic weight from the West to the East and to satisfy the infrastructure gap in the region.

China’s Connectivity Drive and its three-Pronged Strategy

According to the International Monetary Fund (IMF),China overtook the US in 2014 to become the world’s largest economy in terms of Purchasing Power Parity (PPP). 1 This makes China accountable for 16.5 per cent of the global economy, compared to 16.3 per cent for the US. In nominal terms, though, China’s economy is still US$7.0 trillion smaller than the US, and is not likely to overtake the latter for quite some time. In 2013, China surpassed the US in terms of global trade. Its annual trade in goods passed the US$4 trillion mark vis-à-vis US’ US$3.8 trillion. China’s real Gross Domestic Product (GDP) growth has been the fastest among all major economies in the world, averaging close to 10 percent over the last two decades. China is also a major player in world currency and financial markets. It holds US$4.0 trillion in foreign exchange reserves, much higher than world number two, Japan with US$1.3 trillion.

As against this, the US economic position in terms of GDP and other key indicators have been faltering. Although after the 2008-09 crisis, the US economy, in terms of real GDP, began to recover, the pace of growth remained slow and uneven. Much of the sources of growth came from transitory factors of inventory increase and fiscal stimulus. Moreover, while the capital markets have recovered from its 2008-09 lows, and the employment has increased moderately, significant economic weakness can still be observed in the balance sheet of households, the labour market, and the housing sector. 2 These have consequences not only for confidence in US’ economy domestically but also for its influence abroad. 3 One such policy where the US seems to be losing its leadership is the trade deal of Trans Pacific Partnership (TPP). This trade pact that President Obama spearheaded since 2012 for deepening US’ partnerships in strategic regions, is currently struggling to have domestic support, thereby delaying the adoption of Trade Promotion Authority (TPA) legislation. TPA is a ‘fast track’ procedure that pre-commits the US Congress to implement legislation, without amendment and within a specified time frame. In absence of the legislation, the negotiation among the 12 Asia-Pacific countries is likely to fail, generating doubts on US’ credibility and its ability to make rules in international trade. 4 It is in this flux that China is emerging as a dynamic player in the global economy.

Disclosing the Physical Routes

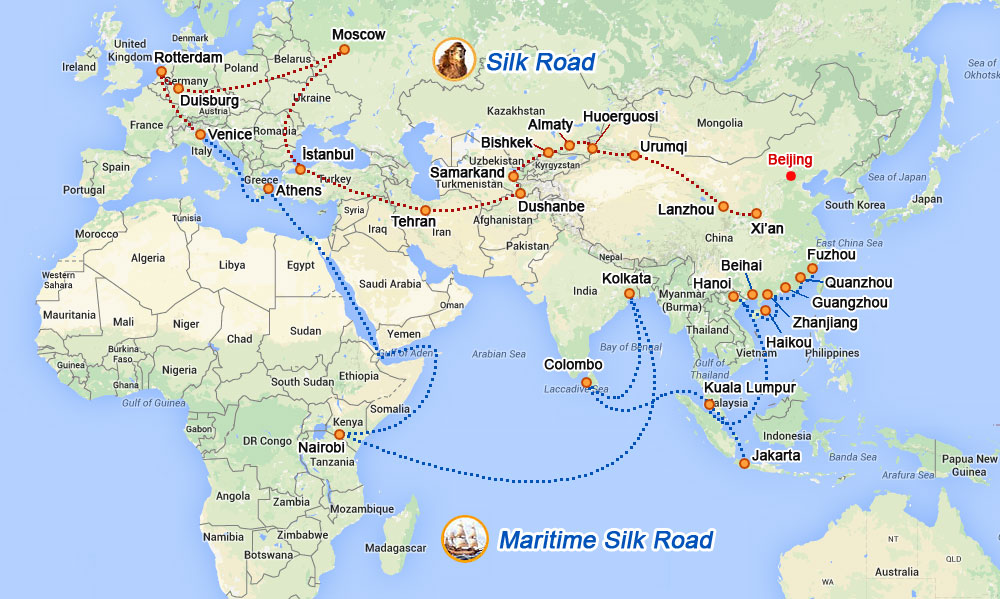

China announced its ‘One Belt, One Road’ initiative in 2013, referring to the New Silk Road Economic Belt, which was said to link China with Europe through Central and Western Asia; and the 21st Century Maritime Silk Road, which was to connect China with Southeast Asian countries, Africa and Europe (Map shown below).

The core objective of the initiative is to encourage the Chinese firms to venture into emerging economies that already have trade and investment linkages with China. The initiative underlines the government’s initiative to share China’s development experience, leverage on China’s development assistance and to export China’s technologies and production capacity in oversupplied areas such as steel manufacturing. 5 These plans are expected to put China at the centre of Asian trade and transport.

It should be noted that, as of 2014, China accounts for 11 per cent of the global merchandise trade of US$38 trillion. As most of the international trade happens through shipping routes, China is a major source and destination of international shipping routes. According to the World Shipping Council, in 2013, seven of the top ten container ports are in China, with the port of Shanghai being the world’s largest. 6 The country is the largest ship-building nation and has three shipping companies that are among the largest container transporters. 7 In addition, increasingly Chinese firms are venturing into construction and management of ports in other parts of the world (like in Sri Lanka, Pakistan, Nigeria, Togo, Greece, Belgium). 8 Against this background, it is not surprising that China wants to play an increasing role in regional connectivity plans.

Financing Plan

The second aspect of China’s three-pronged strategy is the instruments through which the country aims to finance these plans. A Silk Road Fund worth US$40 billion has been set up to start investment in infrastructure, energy resource development, industrial cooperation and other projects related to connectivity for countries along the ‘Belt and Road’ initiative. 9 The initial capital of the fund is kept around US$10 billion, which has been decided to be sourced from foreign exchange reserves (65 per cent) and three other institutions, namely the Export-Import Bank of China (15 per cent), China Investment Corporation (15 per cent) and China Development Bank (5 per cent). 10

In addition to this Fund, there are two proposed multilateral lending banks—the Asian Infrastructure Investment Bank (AIIB) and the BRICS New Development Bank (NDB). The AIIB was first proposed by the Ministry of Finance of China in early 2013. On October 24, 2014, 21 members – China, India, Thailand, Malaysia, Singapore, the Philippines, Pakistan, Bangladesh, Brunei, Cambodia, Kazakhstan, Kuwait, Laos, Myanmar, Mongolia, Nepal, Oman, Qatar, Sri Lanka, Uzbekistan and Vietnam – entered into a MOU to establish AIIB. Subsequently, another 35 countries have joined or expressed their interest in joining the bank, including Australia, New Zealand, UK, France, Germany, Italy, Switzerland, Luxembourg, South Korea, Hong Kong, Taiwan and Canada.

The authorised capital of AIIB is US$100 billion, with 50 per cent or US$50 billion to be contributed from the foreign reserve of China. The registered capital has been decided to be contributed by members in instalments, the first being only 10 per cent (or US$5 billion). The signing of MOU and confirmation of holdings of the AIIB are likely to be completed by June 2015. The bank is expected to commence its operation in Beijing by the end of 2015. 11

For the BRICS’ New Development Bank (NDB), it was agreed between Brazil, Russia, India, China and South Africa so as to provide financing to the infrastructure and development projects of the members and other developing countries. The authorized capital of BRICS Bank is US$100 billion, with an initial capital of US$50 billion in place. The five BRICS economies will have equal stakes in the Bank. The bank will be established in 2016 with its head office will be in Shanghai. The last capital pool for the ‘Belt and Road’ initiative is the Shanghai Cooperation Organization Development Bank that includes members like China, Russia, Kazakhstan, Kyrgyzstan, Tajikistan and Uzbekistan. In this way the four capital sources cover almost all the countries along the ‘Belt and Road’ projects.

Feasibility of the Physical Routes

The third facet of the Chinese connectivity strategy is to make the announced physical routes viable by increasing the volume of trade and investment along the routes. It should be noted that China announced the Silk Road Fund and arranged the signing-in ceremony of AIIB in Beijing a few days ahead of the 21-member Asia Pacific Economic Cooperation (APEC) Summit. During the APEC Summit, China actively pushed for the Free Trade Area of the Asia-Pacific (FTAAP) among APEC countries and finally got the member economies to agree to a ‘strategic study’ to be delivered by 2016. The idea of an FTAAP was first suggested in 2004 and a feasibility study was undertaken in 2006. However, there has been no concrete decision on what pathways to use to achieve an FTAAP and the timing of such an arrangement. But in 2014, again under China’s chairmanship, FTAAP was revived. An FTAAP with current APEC membership is said to create the largest free trade area in the world that has great potential for improving welfare of participating economies and for boosting economic growth in the region. 12

Overall, many regarded these three-pronged Chinese initiatives as strategic moves to counterbalance US’s 2011 announcements of ‘Pivot to Asia’ and the launch of Trans Pacific Partnership negotiation in absence of China’s membership. 13 During the 2014 APEC Summit, President Xi Jinping presented his vision for an ‘Asia Pacific dream’ of shared development and prosperity with concrete proposals and resources that China is ready to put forward to realise it. 14 With promise of around US$240 billion of funding through new multilateral infrastructure lending bank and Silk Road Fund, Beijing used its APEC year of Chairmanship to disclose the routes of the ‘Belt and Road’ initiative, connecting Asia to the Pacific and advance progress toward a region-wide Free Trade Area of the Asia-Pacific (FTAAP). In doing so, China informed the global community that ‘China has the capability and the will to provide more public goods to Asia-Pacific and the whole world.’ 15

Why a China-driven Asian Infrastructure Investment Bank (AIIB)?

There is a significant need of infrastructure development among Asian countries and related to it is a huge need for long-term financing. According to the Global Competitive Report 2014-2015, published by the World Economic Forum, the average score for infrastructure availability and quality among the developing countries of Asia is around 4.0 (Table 1). 16 This is against a score of 6.0 for the United Kingdom, 5.9 for Japan and 5.8 for the United States. In addition, there is a wide variation in infrastructure availability and quality across the countries. While Singapore, Hong Kong and South Korea are among the top ten of the 138 countries being ranked; Indonesia, India are in the middle with ranks in the 60s; and Nepal and Myanmar are almost at the bottom.

Table 1: Infrastructure Availability and Quality (out of 138 countries)

| RANKING | COUNTRY | SCORE (1-7) | RANKING | COUNTRY | SCORE (1-7) | |

|---|---|---|---|---|---|---|

| 1 | Singapore | 6.1 | 83 | Sri Lanka | 3.5 | |

| 2 | Hong Kong | 6.0 | 89 | The Philippines | 3.4 | |

| 7 | Korea | 5.8 | 94 | Pakistan | 3.3 | |

| 15 | Taiwan | 5.5 | 101 | Cambodia | 3.1 | |

| 23 | Malaysia | 5.1 | 109 | Bhutan | 3.0 | |

| 36 | China | 4.6 | 115 | Laos | 2.9 | |

| 46 | Thailand | 4.3 | 119 | Bangladesh | 2.8 | |

| 60 | Vietnam | 3.9 | 123 | Nepal | 2.7 | |

| 64 | Indonesia | 3.9 | 136 | Myanmar | 2.1 | |

| 67 | India | 3.8 | ||||

| AVERAGE | 3.9 |

In another study by the Asian Development Bank (ADB), it estimates that from 2010 to 2020, Asia’s overall national infrastructure investment needs will be US$8 trillion. Out of this, 68 per cent is for new capacity investments and 32 per cent is for maintaining and replacing existing infrastructure. Hence, on average the infrastructure investment need is expected to amount to about US$730 billion per year (Table 2). In addition, the region will need to spend approximately US$300 billion on regional pipeline infrastructure projects 17 in transport, energy, and telecommunications. Altogether, there will be an infrastructure investment need of about US$750 billion per year during this 11-year period. 18

Table 2: Asia’s Total Infrastructure Investment Needs, 2010-2020 (in 2008 US$ billion)

| New Capacity | Replacement | Total | |

|---|---|---|---|

| Energy (Electricity) | 3167 | 912 | 4088 |

| Telecommunications | 325 | 730 | 1055 |

| Transport | 1762 | 704 | 2466 |

| Water & Sanitation | 155 | 226 | 381 |

| TOTAL | 5419 | 2573 | 7992 |

All these studies raised concerns on need for infrastructure in the region and accordingly in the last few years, regional groupings, like the Association of Southeast Asian Nations (ASEAN) and the Asia-Pacific Economic Cooperation (APEC), came up with their regional connectivity plans. While the ASEAN countries adopted the Master Plan of ASEAN Connectivity in 2010 and also instituted an ASEAN Infrastructure Fund of US$485.2 million in equity contribution and US$162 million in hybrid capital, the fund is too small to address the infrastructure gap in the region. Even though the public-private-partnership (PPP) mode of financing has been encouraged repeatedly, the ASEAN region lacks experience in developing and implementing cross-border and bankable projects.

Hence, the rationale for the AIIB has been built focusing on the major needs of infrastructure financing in the Asian region. For the existing multinational financing institutions, like the Asian Development Bank (ADB) and the World Bank (WB), although they have a capital base of around US$160 billion and US$223 billion respectively, much higher than the current size of AIIB’s, the loan support extends to everything from environmental protection to poverty alleviation and to gender equality. 19

With the authorised capital of US$100 billion, the AIIB is likely to be one of the largest multilateral development banks (MDBs) in the world, following the European Investment Bank (EIB), the WB, the Inter-American Development Bank and the ADB. It is estimated that based on the lending to capital ratios of the EIB and the WB, the AIIB could extend loans from 100-175 per cent of the authorised capital (US$100 to US$175 billion). Assuming all is invested in the Asia-pacific infrastructure, this is 4 per cent of US$750 billion estimated by the ADB. However, with the desire to leverage on Public –Private-Partnership (PPP) at a later date, this amount could grow much bigger. 20

A more strategic reason for an Asia-led infrastructure finance institution is the mismatch between the contribution of the developing economies to global GDP growth and their voting rights in the existing MDBs. For example in the IMF, with a combined share of world GDP of 24.5 per cent, economies like China, India, Brazil and Russia command only 10.3 per cent of the votes. However, with 13.4 per cent of world GDP, the four European economies – France, Germany, Italy and the UK – command 17.6 per cent of the votes. 21

One last rationale for a China-driven infrastructure financing plan is the use of the country’s huge foreign exchange reserves. As of end-2014, China holds around US$4 trillion of such reserves, accounting for almost half of the country’s GDP. While part of the reserves have to meet the safety and liquidity management issues, maintain exchange rate stability and prevent financial risks, the rest can be deployed for supporting national economic development and promoting international financial cooperation.

Safety and liquidity concerns are the reason most countries, including China, hold significant reserves in US treasuries and bank deposits. For example, as of the third quarter of 2014, US government debt accounted for 32.6 per cent (US$1.3 trillion) of China’s foreign exchange reserves. However, US yields have been low for a considerable period due to the accommodative policy of the Federal Reserve and the continued dovish stance of players in the financial markets. Hence, in order to meet value preservation and appreciation objectives of the reserves, investments in capital markets and the real economy in the form of long-term debt and equity are becoming necessary. In recent years, China has been actively looking for options for its foreign exchange reserve usage. Some examples are asset-injections in state-owned commercial banks in 2003, bilateral currency swap arrangements with trade partners, aid to countries in crisis, participation in the IMF reforms and establishment of the Sovereign Wealth Fun (SWF). 22 But China still needs many other ways to make good use of its foreign exchange reserves. In this context again, AIIB is a key tool.

Conclusion

The issue of connectivity – ports, highways, railways, pipelines, and telecommunication – has gained global momentum since early-2014. Although the discussion started with the 2010 Master Plan of ASEAN Connectivity, followed by the 2013 APEC Connectivity plan, China soon came at the forefront by launching its ‘Belt and Road’ initiative and its related financing and international trading plans (FTAAP) during its chairmanship year of APEC meetings.

Indeed, there is a need for financing infrastructure projects in the Asian region. This occupies paramount importance in the domestic policies of countries as infrastructure is a pre-requisite for sustainable economic growth, development, inequality as well as inclusion of all strata of society. Moreover, the countries are part of multiple trade and investment agreements, with an objective of reduction in cross-border transaction costs and facilitation of movement of goods among the member countries. The current financing institutions that are present in the region are either inadequate to address the resource gap or have predominant focus on poverty reduction and other social development.

Despite a lot of activity by China in 2014 keeping in mind both the regional and its own interests, things are still fluid. Lately, infrastructure financing modes are observing heightened competition in the form of NDB, AIIB and the WB promoted Global Infrastructure Facility. 23 But as the efforts are still a work in progress, there is increasing discussion on these new facilities, especially of the AIIB and its governance structure, the voting and decision-making rules and its ability to get past scrutiny on environmental, labour and gender issues. While the US is still concerned about the formation of AIIB, many of its allies, including Britain, Germany, France and New Zealand have joined as founding members and the World Bank and the IMF have openly endorsed it and have announced their cooperation with the China-proposed institution. 24 Moreover, the strategic study on FTAAP is not yet complete and as the name says ‘strategic’ and not ‘feasibility’, there is no hint of a start of negotiation anytime soon. It may get even lesser attention if TPP gets signed later this year in 2015.

Of course, as it is still very nascent, AIIB is unlikely to compete directly with the existing institutions of ADB or WB that are more established and have a long track record. However, if it is set up properly, AIIB could offer a novel new alternative for financing the Asian infrastructure needs. There is of course apprehension around China’s economic rise for many countries both in the developed and developing worlds, and all actions as the AIIB is nurtured will be followed very closely. Any step that is not transparent in nature may attract criticism and will slow down the entire process. It is a tight rope that the Chinese government will have to walk carefully, if they want to play a leading role in the journey for Asian connectivity.

Sanchita Basu Das

Sanchita Basu Das is an ISEAS Fellow and Lead Researcher (Economic Affairs) at the ASEAN Studies Centre, ISEAS, Singapore.

Kyoto Review of Southeast Asia (Issue 17), Young Academics Voice, June 2015

Notes:

- Purchasing Power Parity is used to compare the income levels in different countries. It determines the adjustments needed between the exchange rates of two currencies to make them at par with the purchasing power of each other. In other words, the expenditure on a similar commodity must be same in both currencies when accounted for exchange rate. ↩

- Elwell, Craig K. (2013) ‘Economic Recovery: Sustaining US Economic Growth in a Post-Crisis Economy’, Congressional Research Service, April 18 (https://www.fas.org/sgp/crs/misc/R41332.pdf; accessed on 14 May 2015) ↩

- Bremmer, Ian (2014). ‘The Tragic Decline of American Foreign Policy’ The National Interest, April 16 (http://nationalinterest.org/feature/the-tragic-decline-american-foreign-policy-10264; accessed on 14 May 2015) ↩

- Solis, Mariya. (2015) The Geo-Political Importance of the Trans-Pacific Partnership – At Stake a Liberal Economic Order, March 13 (http://www.brookings.edu/blogs/order-from-chaos/posts/2015/03/13-geopolitical-importance-transpacific-partnership, accessed on 14 May 2015) ↩

- One Belt, One Road, Caixin Online, 12 October 2014 (http://english.caixin.com/2014-12-10/100761304.html); The AIIB: China’s Rising Influence in Asian Development Finance, ANZ Research, 26 March 2015. ↩

- World Shipping Council, Top 50 World Container Port (http://www.worldshipping.org/about-the-industry/global-trade/top-50-world-container-ports; accessed on 14 May 2015) ↩

- UNCTAD, Review of Maritime Transport 2013, pp. 58–59. and ‘Top 100 Existing Fleet in February 2015’, (http://www.alphaliner.com/top100/) ↩

- China’s Foreign Ports: The New Masters and Commanders, The Economist, July 8, 2013 (http://www.economist.com/news/international/21579039-chinas-growing-empire-ports-abroad-mainly-about-trade-not-aggression-new-masters; accessed on 14 May 2015) ↩

- China Pledges US$40 billion for Silk Road Plan, Outlook, November 8, 2014 (http://www.outlookindia.com/news/article/China-Pledges-USD-40-Bn-for-Silk-Road-Plan/867047) ↩

- Where will the funds come from for the Belt and Road Strategy?, China Merchant Securities (HK) Co Ltd, Macro Report, January 16, 2015. ↩

- One Belt, One Road, Caixin Online, 12 October 2014 (http://english.caixin.com/2014-12-10/100761304.html); The AIIB: China’s Rising Influence in Asian Development Finance, ANZ Research, 26 March 2015. ↩

- Kim, Sangkyom; Park, Innwon and Park, Soonchan (2013), ‘A Free Trade Area of the Asia Pacific (FTAAP): Is it Desirable?’, Journal of East Asian Economic Integration, Vol. 17, No. 1, pp. 3-25. (http://www10.iadb.org/intal/intalcdi/PE/2013/11844.pdf) ↩

- Mark E. Manyin et al, Pivot to the Pacific? The Obama Administration’s “Rebalancing” Toward Asia, Congressional Research Service (http://www.fas.org/sgp/crs/natsec/R42448.pdf); Sanchita Basu Das, The Trans-Pacific Partnership as a Tool to Contain China: Myth or Reality? ISEAS Perspective, 17 May 2013 (http://www.iseas.edu.sg/documents/publication/ISEAS_perspective_2013_31-the-tpp-as-a-tool-to-contain-china-myth-or-reality.pdf) ↩

- ‘Chinese dream’, Xi Jinping outlines vision for ‘Asia-Pacific dream’ at Apec meet, South China Morning Post, China, 10 November 2014 (http://www.scmp.com/news/china/article/1635715/after-chinese-dream-xi-jinping-offers-china-driven-asia-pacific-dream?page=all) ↩

- China Sees Itself at Center of New Asian Order, The Wall Street Journal, 9 November 2014 http://www.wsj.com/articles/chinas-new-trade-routes-center-it-on-geopolitical-map-1415559290 ↩

- World Economic Forum, The Global Competitiveness Report 2014-2015 (http://www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2014-15.pdf) ↩

- Regional Infrastructure Projects are defined as (i) projects that involve physical construction works and/or coordinated policies spanning two or more countries, (ii) national infrastructure projects that have a significant cross-border impact ↩

- ADB and ADB Institute. 2009. Infrastructure for a Seamless Asia. Manila ↩

- Why China is creating a new World Bank for Asia, The Economist, November 11, 2014 (http://www.economist.com/blogs/economist-explains/2014/11/economist-explains-6; accessed on 14 May 2015) ↩

- The AIIB: China’s Rising Influence in Asian Development Finance, ANZ Research, 26 March 2015 ↩

- Wade, R and Vestergaard, J. (2014), The IMF Needs a Reset, International New York Times, 5 February (http://www.nytimes.com/2014/02/05/opinion/the-imf-needs-a-reset.html?_r=0) ↩

- Where will the funds come from for the Belt and Road Strategy?, China Merchant Securities (HK) Co Ltd, Macro Report, January 16, 2015. ↩

- Global Infrastructure Facility is promoted by the World Bank to facilitate complex infrastructure projects in October 2014 (http://www.worldbank.org/en/news/press-release/2014/10/09/world-bank-group-launches-new-global-infrastructure-facility) ↩

- World Bank Chief Endorses Rival AIIB, The Financial Times, April 7, 2015 (http://www.ft.com/cms/s/0/c58cbd66-dcee-11e4-975c-00144feab7de.html#axzz3XAnNkhwY); IMF happy to Cooperate with China on AIIB, March 22, 2015, Reuters (http://www.reuters.com/article/2015/03/22/us-china-imf-idUSKBN0MI06J20150322) ↩